Volkswagen Infinity Squeeze. The October 2008 short squeeze on shares of Volkswagen AG has since been referred to as the “Mother of all Squeezes”. It was also perhaps the earliest use of the term “Infinity Squeeze”. It was during the middle of the worst financial crisis since the Great Depression, and Volkswagen was increasingly being viewed as a potential bankruptcy candidate. In other words, Volkswagen was viewed as an exceptionally attractive short candidate. However, at very depth of the crisis, an orchestrated short squeeze on VW shares caused VW to briefly become the most valuable company in the world, worth more by market cap than Exxon Mobil.

The VW infinity squeeze seemed entirely counter intuitive at the time. And that is exactly the point. All infinity squeezes are the result of heavy over-shorting of shares which then become difficult or impossible to cover. Such aggressive over-shorting only occurs when the bear thesis against the fundamentals is conclusively strong and very well disseminated. In other words, stocks which appear to be the “best short ideas” are also the ones which often end up being most likely to see the most violent short squeezes.

At the peak of the Great Financial Crisis in October 2008, Volkswagen had been (rightfully) viewed as a high probability bankruptcy candidate. Even before the crisis, heavily indebted VW had already been struggling financially, and in the midst of a crisis, demand for new cars would surely plummet. Despite its troubled financials and business prospects, VW had reported several quarters of slightly better than expected earnings, leaving its share price surprisingly elevated at over €300. Combined, these factors made VW a seemingly very attractive short candidate as the financial crisis unfolded in 2008.

In fact, as the financial crisis unfolded in 2008, the entire auto sector was considered to be a highly attractive short trade. As a reminder, up until 2008, General Motors had been the largest automaker in the world for more than 70 years and had over 200,000 employees. But by December 2008, GM was being bailed out by the US government and by 2009 GM had entered bankruptcy. Automaker Chrysler would file for bankruptcy at roughly the same time in 2009. Against this backdrop, in late 2008 a short bet on troubled Volkswagen seemed like an absolute no brainer.

- How General Motors Was Really Saved: The Untold True Story of The Most Important Bankruptcy In U.S. History (Forbes, Nov. 2013)

- Why Did Car Sales Drop So Dramatically During the Financial Crisis? (Kellogg School of Management, Apr. 2016)

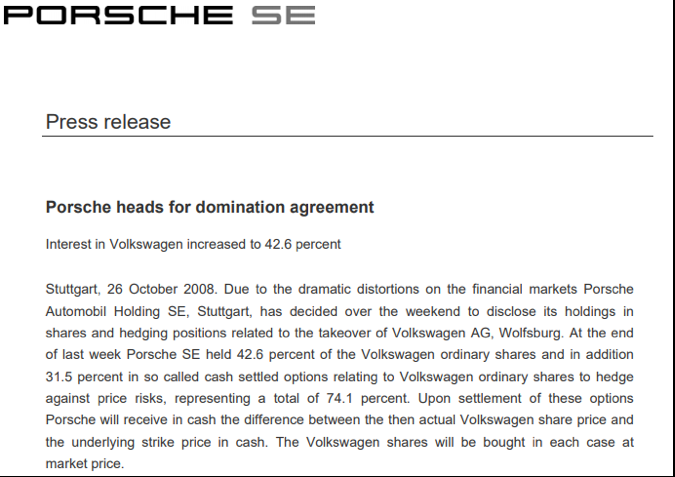

Catalyst for the Volkswagen squeeze. On October 26th, 2008, rival automaker Porsche made a surprise announcement that it had increased its stake in VW to over 74%. It was a stealth move, made possible through the use of multiple purchases of cash-settled derivatives which had been accumulated separately through different European investment banks.

- Porsche heads for domination agreement (Porsche PR, Oct. 2008)

Prior to 2008, Porsche had already been a significant shareholder in VW. Then in October 2008 Porsche took its stake to 30%, even getting board approval to ultimately take that stake to over 50%. However, statements from Porsche at the time had led most investors to believe that Porsche would not be attempting a full-blown takeover.

And in any event, during the financial crisis, luxury car maker Porsche was even more financially strained than VW. There seemed to be little risk of Porsche having any realistic ability to corner the market on its much larger rival VW.

“German automaker Porsche announced that it had raised its stake in Volkswagen to 30.9 percent, triggering a takeover bid under a German law requiring a company to bid for the entirety of any other company after acquiring more than 30 percent of its stock. Porsche announced it did not intend to take over VW, but was buying the stock as a way of protecting it from being dismantled by hedge funds.”

- This Day in History (History.com, Nov 2009)

- Porsche Supervisory Board gives Go-ahead for Majority Stake in VW (Porsche SE, March 2008)

Confusion over “short vs. float”. Prior to the announcement from Porsche, and as the financial crisis was becoming more apparent, short interest in VW had been steadily rising. But even by October 2008, the short interest seemed not excessive, at just 12.8% of outstanding shares. But what the market failed to appreciate was that the true availability of tradeable shares to cover those short positions was actually far lower than what many understood.

- Short sellers make VW the world’s priciest firm (Reuters, Oct. 2008)

Prior to October 2008, Porsche alone had already controlled 30% of VWs shares. Next, the government fund of Lower Saxony (the home province of VW in Germany) owned an additional 20% of VW as a strategic stake.

In addition, various index funds owned around 5% of VW due to VWs large weighting in the DAX index. These index funds were required to hold VW in proportion to its weight in the DAX, such that they would not be able to sell simply due to changes in the price of VW. Volkswagen alone made up 17% of the DAX index at the time.

Looking at the above, it is clear that heading into October of 2008, around 55% of VW shares were already unavailable in the market for any realistic purposes. As a result, when Porsche increased its stake by an additional 44%, it meant that the true available float went down from 45% of outstanding shares to around just 1% of outstanding shares. Suddenly the seemingly “low” short interest of 12.8% turned in to a massive supply and demand imbalance. Millions of shares needed to be bought immediately even though there were simply no shares available to be sold.

Just to ensure that short sellers fully understood the urgency of their calamity, Porsche made sure to include in its announcement a few words to address the short position.

Porsche stated that they had:

“decided to make this announcement after it became clear that there are by far more short positions in the market than expected.”

Porsche added that:

“the disclosure should give so called short sellers – meaning financial institutions which have betted or are still betting on a falling share price in Volkswagen – the opportunity to settle their relevant positions without rush and without facing major risks.”

Despite the disarming choice of wording, the statement from Porsche had precisely the effect that anyone would have expected. The announcement triggered a mass panic for the exits by anyone who was short shares of VW.

Porsche had also made this announcement on a Sunday, when the market was closed. As a result, the message would be widely disseminated at a time when short sellers would have zero ability to cover their positions until the market reopened.

Note: Seven years after the VW infinity squeeze, Martin Shkreli would make use of nearly identical tactics and timing when orchestrating a 10,000% short squeeze on KaloBios (KBIO). Shkreli made his explosive announcement on Thanksgiving day, when markets were closed.

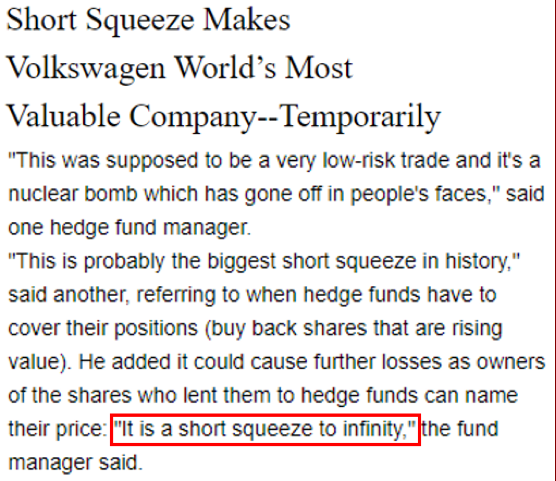

The VW Infinity Squeeze. Following the announcement by Porsche, the resulting panic caused a short squeeze in VW shares that saw the deeply troubled automaker briefly become the most valuable company in the world – despite being in the middle of the worst financial crisis since the great depression. VW’s share price briefly exceeded €1,000 intraday with a market cap of over €300 billion.

- Short sellers make VW the world’s priciest firm (Reuters, Oct. 2008)

- Porsche and VW: how Germany got revenge on hedge fund ‘locusts’ (Telegraph, Oct 2008)

- VW goes from the Beetle to the world’s most valuable company (The Guardian, Oct. 2008)

- Panicked Traders Take VW Shares on a Wild Ride (The New York Times, Oct. 2008)

Porsche wins. Everyone else loses. Big. As a result of its skillful financial engineering, Porsche netted itself more than $10 billion in profits in a matter of just a few short weeks. It was money that was badly needed by Porsche. Luxury car sales were plunging due to the crisis and Porsche was already saddled with significant debt.

On the other side of the trade, the hedge funds who had sold VW short quickly saw their collective losses exceed $30 billion. Hedge fund managers were “literally in tears on the phone” as they described “a nuclear bomb going off in our faces.”

As a mega cap company, the short sellers who had been involved in the VW trade included some of the best-known names in the hedge fund industry. This included David Einhorn of Greenlight Capital, Andreas Halvorsen of Viking Global, Paul Singer of Elliott Management, Glenn Krevlin of Glenhill Capital, Crispin Odey of Odey Asset Management, among others. SAC Capital’s Steve Cohen had said that his fund alone had lost $250 million in just one week on VW.

- Steve Cohen Tells Paul Tudor Jones About Two Worst Days of His Life (Business Insider, Feb. 2011)

Various funds would end up filing civil suits against Porsche to attempt to recover their losses. But ultimately there would be no significant consequences to Porsche.

- Hedge Funds Seek $2.4Bn Damages from Porsche’s Owning Family (Business Insider, Feb. 2014)

- Hedge funds’ $1.4 billion Porsche lawsuit faces dismissal: judge (Reuters, Feb. 2015)

- Porsche Holding Wins Hedge Fund Lawsuit at Germany’s Top Court (Industry Week, Dec. 2016)

Know yourself, know your opponent. (A hedge fund that made a few sports cars on the side.)

Markets will always be full of surprises. But in 2008, the actions by Porsche should likely not have come as a complete surprise. In fiscal 2007 Porsche earned three times as much money from trading derivatives as it did from selling cars, and most of these derivatives were on shares of VW. Of Porsche’s €5.86 billion in pre-tax profits in 2007, €3.6 billion was from options trading, with only €1.05 billion from selling cars.

Porsche’s derivative trading activities were entirely obvious to the market and had even drawn criticism from sell side analysts. Analyst Stephen Cheetham of Sanford Bernstein said of Porsche, “It does look like a hedge fund.” Another analyst said, “It is a hedge fund investing in just one stock.”

- Porsche makes more money from options trading than from cars (Foreign Policy, Nov. 2007)

- VW options power Porsche profits (Financial Times, Nov. 2008)

- Porsche: The Hedge Fund that Also Made Cars (Pricenomics)

- Short Squeeze Makes VW World’s Most Valuable Company–Temporarily (Autobody News, Oct 2008)

As a result of the squeeze on VW in 2008, Porsche made eight times more from options trading than it had made from its “core” business of selling cars.

Stone Cattle Road. As a observation, if someone really wanted to make Mexico pay for a gigantic wall on its northern border, the last thing one would do is go out and publicly tell everyone that this was their intention.

Likewise, when Porsche set out to eviscerate the short sellers, Porsche made it a point (prior to the final announcement) to clearly downplay in public that it had any such intention of actually taking over VW. No one should have expected that Porsche to come out and advertise any intentions.

- This Day in History (History.com, Nov 2009)

- https://en.wikipedia.org/wiki/Stone_Cattle_Road

“Show me the incentive, I will show you the outcome”. In retrospect, Porsche’s activities were somewhat predictable based on the incentives that had been given to its CEO. When Porsche CEO Wendelin Wiedeking came aboard in 1993 he was able to negotiate a contract that gave him almost 1% of the company’s annual pre-tax profits as a bonus.

At the time of Wiedeking’s contract in 1993, Porsche was losing $150 million per year. In 2008, as a result of the VW infinity squeeze, Porsche earned a bottom line profit of nearly €7 billion.

For 2008 alone, CEO Wiedeking received a bonus of €80 million. He was then “pushed out” of Porsche in 2009, but was given an additional bonus of €50 million on his way out.

- Porsche chief executive pushed out with €50m payoff (The Guardian, July 2009)

- Has Porsche Bitten Off More than It Can Chew? (Spiegel Online, Apr. 2009)

- Porsche Fails to Swallow VW (Spiegel Online, May 2009)

At the time of Wiedeking’s departure in 2009, Porsche was now saddled with $19.8 billion in debt, primarily related to the pursuit of VW. Interest payments alone were $790 million per year and Porsche needed $10 billion in debt refinancing at a time when banks were now closed to lending new money.

However, by the end of 2009, Wiedeking had made the cover of Fortune magazine, being named “European Businessman of the Year”, sharing the cover with a mention of Steve Jobs.

Conclusion. Over the longer term, VW’s share price ended up falling significantly. And over the long term, this outcome was certainly quite predictable. But from a financial standpoint, investors who shorted VW shares at what appeared to be the optimal time suffered very steep trading losses. Ultimately, the only thing that matters to investors is realized gains and losses. The market places zero value on any post dated “I Told You So”.

TIMELINE-Porsche’s pursuit of Volkswagen (Reuters, Jan. 2011)