Past Reports

Update from Moxreports

August 21, 2020

Dear all, I am still “stuck” in Bali due to travel difficulties around COVID, but I expect to be back to LA in the next few weeks, travel permitting. Either...

Long PLCE and SCVL. Watch for more bounces on oversold “BaMRs”

October 16, 2019

This report is the opinion of the author. The author is long PLCE and SCVL. See disclosures and disclaimers. Summary. Throughout 2017, 2018 and 2019, my best performing strategy has...

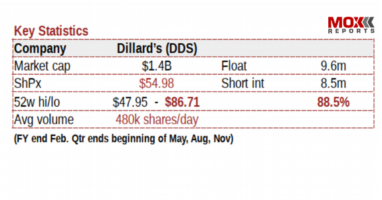

Long DDS. Watch for the (as usual) violent rebound. Here’s the catalyst.

August 28, 2019

As a result of Dillard's hyper-aggressive share buyback, short interest now amounts to 88.5% of the remaining float

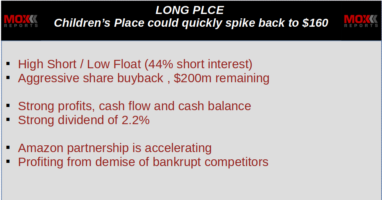

Long PLCE. Children’s Place could quickly spike back to $160

August 1, 2019

Short interest recently hit 44%, even as the company continues to buy back shares. Children's Place has been buying up the assets of bankrupt competitors and is the sole provider...

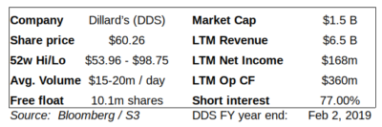

Dillard’s (DDS) could quickly double on “upside perfect storm” (LONG DDS)

June 24, 2019

Dillard's short interest just jumped to 77% even as the ongoing buyback continues to shrink the float. Despite lackluster earnings, Dillard's has very strong cash flow to continue the aggressive...

Moxreports 2.0

June 16, 2019

Welcome to the new Moxreports. Please have a look around. Comments are welcome.

Behind the scenes with Vuzix, Sichenzia and IRTH

April 22, 2019

By necessity, the material in this report revolves around me. You will also see significant detail about heavily promoted public companies and their law firms, stock market “financiers” and “investor...

Long REV. Revlon’s short vs. float setup just became tighter than Tilray(TLRY)

September 19, 2018

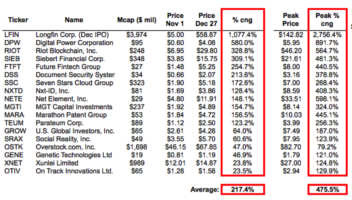

Shares of Tilray (TLRY) have now spiked up by more than 10x from its recent IPO price. The reason is simply that the short interest became too high relative to...

Long BITA. Here’s how Bitauto (BITA) rises to $240

July 10, 2018

Bitauto (BITA) is a heavily shorted, low float stock but there is far more to the bull case than a simple short squeeze. As with my long report on RH...

Long REV. Missed disclosure changes point to Revlon buyout

June 7, 2018

Much of the information in this report appears to have been entirely missed by the market. Only 5-10% of Revlon’s shares are in the public float. Only a single analyst...

Long PLSE. Here’s why Pulse is headed sharply higher

May 8, 2018

Pulse is scheduled to discuss “Operational Highlights” on a conference call at 4:30 pm today (Tuesday May 8th). In the past I have highlighted such calls which companies used to...

Short VUZI. Fraud.

March 16, 2018

This report is the opinion of the author. The author is short VUZI. Vuzix recently used an undisclosed stock promotion involving dozens of mainstream media outlets to artificially inflate the...

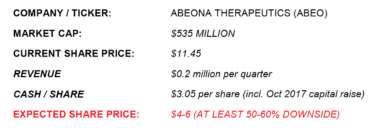

Short ABEO. Short Abeona on Manipulated Trial Data

February 15, 2018

Summary In Oct 2017, shares of ABEO hit a new high of $19.55 following the release of seemingly positive data in its clinical trial for MPS-III. ABEO quickly used that...

Short EEFT. Euronet To Drop 50-60% On Latest DCC Developments

February 1, 2018

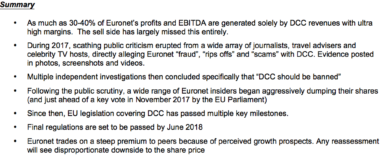

Summary As much as 30-40% of Euronet’s profits and EBITDA are generated solely by DCC revenues with ultra high margins. The sell side has largely missed this entirely. During 2017,...

Long OSTK. Overstock headed sharply higher (despite obvious problems)

January 24, 2018

As of December, short interest in OSTK hit 42%. Latest data will be released after market close today. Given recent activity, I expect short interest to hit 50-60%. The key...

Long GCAP. Why Gain Capital could see a “super spike” today

December 29, 2017

“Dinner Table Effect”. Crypto assets spiked sharply after both Thanksgiving and Christmas. Traders expecting crypto assets to again spike very sharply on Jan 2. In anticipation, traders, funds and algos...

Long GCAP. Bitcoin rollout could send Gain Capital sharply higher

December 28, 2017

Traders from places like China and Korea are being forced off of their own domestic crypto exchanges but still want to pour money into crypto. GCAP now provides an easy...

Short SSTI. ShotSpotter is worse than you thought

November 21, 2017

Summary: In over 20 years SSTI has never generated profits or meaningful cash. Recent IPO simply allows VCs to finally exit positions. Dec 4th lockup expiration on 8 million shares...

Long RH. RH Will Spike Much, Much Higher Very, Very Soon

November 3, 2017

Summary In May, RH quietly awarded its CEO a massive nine figure incentive package to achieve a $150 share price by any means. Two days later RH announced a $700m...

Short HIIQ. Fraud penalties to exceed $100 million and undisclosed “domino effect”

September 11, 2017

Summary New data points: Fraud penalties expected to reach $100 million or more. Other insurers required to cease doing business with HIIQ as part of their fraud settlements. June 2017:...