Shares of Opko Health (OPK) have risen 65% in the past three months as a string of domestic and international acquisitions, along with a greater collaboration with Bristol Meyers (BMY), has opened up numerous new pathways for the company.

Opko’s prospects as a company continue to be bright, however at the current price of around $7.00 the market cap of Opko now exceeds $2 billion.

This is in spite of the fact that Opko has recently disclosed that it does not expect to become profitable in the near term, which implies that massive revenues (as predicted by various authors) are not on the near term horizon.

As shown on the Form 4’s, insiders have now begun selling, with Opko’s VP of Finance and Chief Accounting Officer selling $336,000 of stock on February 1st.

Based on the information below, at any prices above $5.50 Opko is a clear sell. Although at prices of $4.00-$5.00 the stock likely becomes an interesting buy once again.

Even those who are very bullish on Opko’s long term prospects are now leery of the recent run-up and the lofty share price. Various signals are now emerging that the stock is headed for a significant correction.

The signals include the following:

- Insider selling: According to the latest Form 4, on February 1st, Opko’s VP of Finance and Chief Accounting Officer, exercised his options and immediately sold 100% of the shares underlying at $6.72. Total shares amounted to 50,000, resulting in proceeds of $336,000.

- Heavy share issuance by Opko: Opko has been taking advantage of the run-up in the share price to issue 20 million shares for its acquisition of Cytochroma at $4.87 and another 25 million shares via a convertible bond at $7.07. These representsissuance of over 45 million shares all in the month of January alone.

- Negligible buying by Frost: Purchases from Dr. Frost have continued, but the vast majority were in 2012 at prices of $4.00-$5.00. Only 70,000 shares were purchased above $6.00. Dr. Frost’s historical position is greater than 140 million shares.

- Huge overhang from potential sellers: The recipients of shares from recent acquisitions along with the convertible bond shares now create a massiveoverhang of more than 50 million shares.

Author Kevin Quon has been bullish on the stock but also noted in his most recentarticle the market cap has become difficult to justify. The Motley Fool notes that Opko has “received an alarming one-star ranking“, meaning that it is expected to be a notable under performer. Author Josh Ginsberg continues to be bullish on Opko’s business prospects but notably made no evaluation of the share price following the run-up to $7.00 and $2 billion in market cap.

Clearly these comments do not reflect a lack of opportunities for Opko nor do they reflect a lack of faith in Dr. Phillip Frost or Opko management. Just about anyone familiar with Opko or Dr. Frost continues to be bullish on the long tem prospects for the company.

Instead bearish comments are a reflection on Opko’s share price, which has simply moved way too far way too fast and is now due for a meaningful pullback.

Back in November, Cramer noted that the company was a “$4.00 and change” stock but cautioned viewers

don’t jump all over this thing because you will lose money if you chase it up to $5.00 or something silly like that

That was just 10-12 weeks ago and now the stock is as $7.00. On his most recent show featuring Opko, Cramer continued to be positive on the company’s prospects but stopped short of calling it a buy.

The reasons for his restraint are twofold.

First, the $2 billion valuation now creates far more chance of near term downside than further upside.

Second, according to Dr. Frost, Opko’s prospects for drug revenues are looking likely to be 2014-2015 events as opposed to 2013 events. Clinical trials for the various drugs will be completed in late 2013 and in 2014, such that commercialization will occur about a year after that, according to the interview.

While Cramer will telling investors to not chase the stock up to $5.00, Bill Alpert at Barron’s was telling them to sell outright at $4.00. The scathing article from Barron’sstated that Opko was only worth $1.00-$2.00. Alpert cited medical journals which showed that Opko’s diagnostic tests were failing to detect Alzheimers and prostate cancer as planned. Alpert did acknowledge that Opko would likely be presenting investors with other shots on goal in the future, noting:

With Frost’s deep pockets and a dizzyingly diverse project portfolio, Opko will surely have other stories to tell if these diagnostics don’t fly. But prospective investors might want to wait for the validation that comes with real fundamentals.

There are several misconceptions about Opko which are leading some investors to continue bidding up the stock even at prices above $6.00.

The misconceptions are as follows:

- Many investors are under the impression that Dr. Frost has been purchasing alarge volume of shares at over $6.00 when in fact his purchases have been negligible. The benefit of these small purchases is more one of signaling to the market which has caused the share price to continue to rise.

- Revenue forecasts from bullish authors seem to have significantly overestimated the revenue potential for Opko’s drugs and its 4KScore product. For example, authors are consistently predicting that expected revenues from numerous drugs will exceed those of the best selling drugs of all time for the entire industry. With 4K, authors are assuming the the test will sell for triple the price and immediately capture 50% of the market.

- Many investors are pinning their hopes on a continued short squeeze, but the short squeeze on Opko is now fading. The number of days to cover the short position hasfallen from 43 days to just 11 days. Short interest itself has fallen by 30%, such that the covering shorts will no longer be supporting the share price and may now be re-entering the trade as a new short.

In decades past, Dr. Frost enjoyed spectacular success in selling Key Pharmaceutcials and Ivax Pharmaceuticals after the matured into substantial revenue generators.

But investors must keep in mind that his involvement with each of these companies lasted well over 10 years before the companies were in a position to ultimately be sold.

Those who choose to sell Opko on this latest run-up to $7.00 may well have the opportunity to buy back into the stock at prices back in the $4.00-$5.00 range, at which time they can still make a longer term bet if they are speculating on an ultimate sale of the company by Dr. Frost in the years after revenues begin to materialize.

The Dr. Frost Effect

Many investors seem to believe that the purchases by Dr. Frost are so large that they have pushed up the share price of Opko and caused a short squeeze. However this is demonstrably not the case.

Author Kevin Quon recently noted that:

As of January 11, Frost has effectively taken 135,764,800 shares off of the open market… For a company that held a 17.7% short position of the outstanding float, or 24.26 million shorted shares as of December 31, such continual buying pressure by the CEO has put a real pinch on those looking to profit from a decline in the company’s price.

Quon had separately noted that:

Despite having share prices climb nearly 50% in the last 3 months alone, Frost continues to steadily buy large volumes of shares.

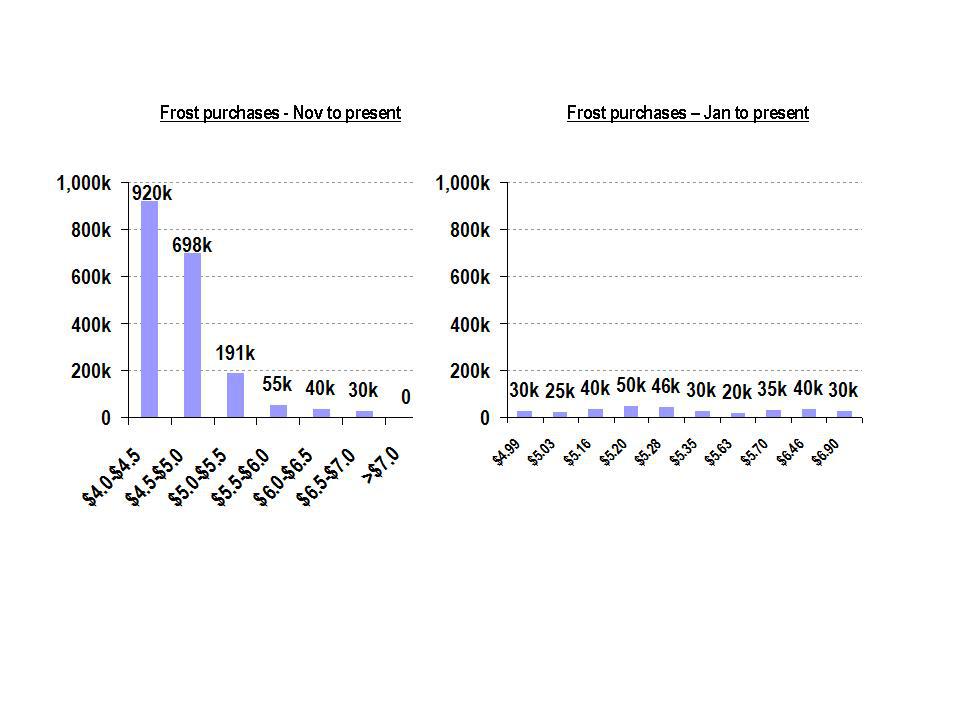

In reality, the volume of shares being purchased by Frost at above $5.00 has actually been entirely negligible, as shown in the chart below. The data comes from the Form 4 filings to the SEC.

The chart on the left shows the volume of shares purchased by Dr. Frost at each price range over the past three months. This is the time period in which the share price has skyrocketed. As we can see, almost all of Frost’s purchases occurred at $4.00-$5.00. There were some purchases even above $6.00, but the volume on these was tiny.

The chart on the right is a subset of the chart on the left and shows the exact prices and volumes of each Dr. Frost’s individual purchases in 2013. As we can see, there have only been a few purchases and the largest one in 2013 so far has been only 50,000 shares.

As a result, it is clear that these purchases are not “large” and are not “pushing up the price” of Opko by themselves. Opko typically trades around 3 million shares per day.

But obviously Frost’s purchases do have a different effect that is distinct from the simple aspect of supply and demand. The real effect here is one of signaling. As Frost continues to buy, retail investors continue to take notice and jump on board with their own buying.

Dr. Frost currently owns over 40% of Opko, with outside institutions owning only 16% of the company. As a result, aside from Dr. Frost, the float is held almost entirely by retail investors.

Investors who pile in at the $6.00-$7.00 level are missing out on the simple economics of why this works for Frost in a way that doesn’t work for anyone else. This may be one of the reasons why institutional ownership continues to be quite low.

Smaller investors need to realize that the result for Dr. Frost has been an increase in ownership of only 0.2% during 2013. His position was already so large that the added shares (even at higher prices) have virtually no impact on his overall cost or on the size of his position.

Dr. Frost invested a mere 0.2% into new shares at higher prices but the signaling value of this boosted the value of his existing 140 million shares by 40%. The economics of this would be nearly identical even if Dr. Frost had purchased the shares at $10.00 or $20.00, so it can be expected that his small purchases will continue for the foreseeable future.

Obviously if the rest of us had the same effect from signaling, we would continue buying small amounts of Opko as well.

If Dr. Frost isn’t selling, then why does he care about the stock price ?

The first point that investors need to realize is that although Dr. Frost isn’t selling shares, Opko is selling frequently and in large size. Opko has already issued over 45 million shares just in the month of January as a result of the Cytochroma acquisition and the convertible bond.

Dr. Frost is using the greatly appreciated stock of Opko as a currency for going on his shopping spree for new companies to acquire.

Prior to the recent interview of Dr. Frost on Cramer, the stock had been at $6.00, however the Cramer effect quickly allowed Opko to issue shares under theconvertible at $7.07.

The disadvantage of the convertible is that it requires $5.25 million per year in interest payment by Opko, totaling $26.25 million in interest for the 5 years in which the bond is not callable by Opko.

Dr. Frost knows that he will continue making acquisitions and he knows he will be issuing much more stock to pay for them. But he is uncertain what the price of the stock will be in coming months, so he was happy to lock in a $26 million interest obligation in exchange for the certainty of issuing equity at $7.07.

As shown above, Dr. Frost made the vast majority of his purchases at prices below $5.00. Only a mere 70,000 shares have been purchased at prices over $6.00. But the signaling effect, along with some help from Cramer, has provided Dr. Frost and Opko with a higher share price for issuing stock in financings and acquisitions.

Mr. Quon also seems to agree with this conclusion, stating that:

By propping up the company’s share price with his own insider purchases, Frost was able to wield greater buying power in the latest acquisitions.

What is the right price to sell Opko stock ?

Obviously the $7.07 conversion price of the convertible says that selling stock at $7.07 is an attractive sale price in the eyes of Opko and Dr. Frost. This appears to be true even though it required paying $26 million in interest.

Just three weeks ago Opko agreed to acquire Cytochroma for an upfront price of $100 million. As in the past, Opko used its stock as currency with 20.5 million shares issuable in lieu of the $100 million. This equates to a share price of $4.87. In addition, there may be an additional payment of up to $190 million, which can also be paid stock if desired.

And now most recently the VP of Finance and Chief Accounting Officer sold 100%of his recently vested options at a price of $6.70-$6.74.

So for those investors who have ridden the stock up, each of these can be viewed as a signal from those who know best that the current level is a time to be sellingrather than buying the stock.

What are the recent acquisitions worth ?

In December Opko closed its acquisition of Prost-Data Inc (OURLab) based out of Nashville. One week later Opko announced that it had acquired Silcon Comércio of Brazil. Within the span of just one month Opko was already on its third deal with Canadian Cytochroma in January.

All three deals do appear to bring significant potential to Opko in the future. But investors do need to realize that doing three major acquisitions in three different countries in just four weeks is a huge amount for any one company to chew on when it comes to integration and implementation.

The current share price seems to reflect a view that completing the three deals on paper is equivalent to having already made them work for shareholders. Investors will need to be patient before expecting results from these recent acquisitions no matter how exciting they are.

In mustering up their patience, investors need to consider that over the past three years Opko has now acquired companies in:

- Mexico

- Israel

- Chile

- Spain

- Canada

- Brazil

- The United States.

Opko had acquired the rights to rolapitant for anti-nausea and vomiting from Schering Plough (MRK) in 2009.

Despite this blistering pace of acquisitions over a three year period, Opko has only just broken through the $10 million mark for quarterly revenues in its most recent quarter.

Rolapitant has been in Opko’s drug portfolio for nearly four years. So again, if these past acquisitions are still works in progress, the most recent acquisitions can be expected to take a few years before they begin to bear the results that investors are currently hoping for.

At $11 million in Q3, revenue growth continues to be impressive relative to where it was in the previous quarter. However, investors need to keep in mind that Opko is not growing these revenues organically, but is instead buying these revenues, using its stock as a currency.

In addition, many investors seem to forget that while each acquisition brings thepotential for new revenues, it also brings the certainty of immediate new expenses related to the deal and all of the new employees that come with it.

Opko has made this point clear. In its most recent 10Q released in November, Opko stated that:

We have a history of operating losses and we do not expect to become profitable in the near future.

Clearly if Opko were expecting even a single billion dollar product to hit the market any time soon, it would be expecting an immediate swing to massive profitability. In its most recent quarter, Opko’s operating expenses totaled only $21 million against revenues of $11 million. An extra billion dollars in expected revenue would obviously change that equation.

In the past Dr. Frost demonstrated his long term focus and extreme patience. Ivax and Key Pharma both took more than 10 years before their revenues grew to a point where they were sellable companies.

Opko currently realizes the time frame which will be required to ramp up revenues as well as the uncertainty which is always associated with bringing new products through the FDA and then into the market. Opko also realizes that it will continue to absorb significantly larger expenses as a result of the acquisitions, even prior to any ultimate revenues which may be realized.

However, despite this clear communication from Opko, many investors are making their own forecasts of surging revenues that will seemingly lead to immediate near term profitability.

A dose of reality – how many billions in revenue ?

Many Opko bulls have predicted that Opko is going to launch a series of new drugs which will each immediately bring in multi-billion dollar revenues.

Opko does have numerous new and attractive shots on goal. Its drugs will certainly address very attractive market opportunities. Yet we can see that this extreme level of optimism is clearly a quite overdone when viewed in the context of the best selling drugs of all time.

Simon King of FirstWord Pharma recently posted a list of the all-time best selling drugs along with the revenue numbers they achieved in their absolutely best peak years.

In order to qualify as one of the best selling drugs of all time across all years, a drug needs to be able to generate peak sales of around $5 billion in any single given year.

A list from the Pharmacy Times shows that the cut off level for the best selling drugs in 2011 was much lower, at $2.7 billion.

In other words, if even one of Opko’s new drug candidates sells $1 billion, it would be going from a base of zero to the pharmaceutical stratosphere immediately.

And in this article, Rich Duprey provides numbers that are far more realistic based on global revenues realized by competing drugs for Replidea and Alpharen (Cytochroma’s drugs). The reality he shows is that competing drugs from Amgen (AMGN) and Sanofi (SNY) which are already established and successful in the market only generate revenues of around $300-$600 million. And the other reality is that it will likely take a number of years to ramp up to that level.

There are two points that the very bullish authors are missing when they provide their mega billions in revenue forecasts. First, there are established drugs which have been competing strongly in the market for many years.

Second, not all individuals with these conditions end up taking drugs. Duprey notes that “surgery is the typical standard of care for secondary hyperparathyroidism”.

As a result, when authors simply start multiplying numbers of sufferers by expected drug prices they come up with spectacular forecasts which end up being far higher than what we see in the real world.

Launching a drug from zero to $300 million in revenues is obviously a major accomplishment. However, in making an evaluation of the current share price, investors need to realize that this level is actually 70-90% lower than what is being predicted by various authors who have set ultra-high expectations of numerous multi-billion dollar drugs.

The dramatic rise in the share price and the $2 billion market cap make it clear that many people are betting that the stock will realize these bullish forecasts even when they are impossible to reconcile with real world revenue potential.

And also of importance is the fact that these revenues are not expected to ramp up until 2015.

Revenue potential is reflected in the acquisition prices

These lower but more realistic revenue projections should not come as a surprise to anyone who has followed the terms of Opko’s acquisitions.

With Cytochroma, Opko issued $100 million in stock up front and may provide up to $190 million in additional payments subject to certain performance milestones.

Cytochroma has two drugs in late stage trials, Replidea and Alpharen. If it were the expectation that these drugs would be pulling in several billion dollars in revenues within the next 2-3 years then they simply would not have sold for a mere $100 million upfront. And in fact there would have been numerous other buyers who would have been happy to bid far more than the $100 million plus $190 million in milestone payments.

The fact is that when an acquirer such as Opko buys a new drug (company), it expects to obtain its payback over the course of several years and it discounts the price based on the uncertainty involved in getting the drug successfully approved by the FDA and accepted by the market.

For Opko, they were willing to pay $100 million upfront, and Cytochroma was willing to accept. If everything goes perfectly, then Cytochroma founders will get an additional $190 million over coming years, if or when the success happens.

Pulling in several hundred million dollars off a newly purchased drug is no small accomplishment and it would certainly be yet another coup for Dr. Frost.

But with a valuation of over $2 billion before the drugs are even through their clinical trials, investors need to ask if the regulatory and commercial success of these drugs is already being priced in before the events have been proven. The sellers of Cytochroma were more than willing to put the value at an immediate $100 million.

A balanced look at 4KScore’s prospects

The nearest term revenue development is expected to be the launch of the 4KScore test for detecting prostate cancer. As a result, it is arguably the most important element for evaluating the current share price and the results are expected to be positive for Opko.

Opko notes that the 4KScore test as “a next-generation prostate cancer test” which “could create a diagnostic test able to accurately predict prostate cancer-positive biopsies”. In addition, Opko notes that 750,000 unnecessary prostate biopsies are performed annually in the US. According to Opko, “A panel combining our PSA test and our novel kallikrein markers could create a diagnostic test able to accurately predict prostate cancer-positive biopsies”.

However Barron’s challenged Opko’s prostate test, saying:

A May 2010 Journal of Clinical Oncology report by the test’s developers claimed that their four-marker test would reduce unnecessary biopsies by half. However, an accompanying editorial in the same issue pointed out that the new screen was less sensitive than existing tests-failing to detect 14% of high-grade cancers-and was not likely to change prostate-cancer mortality.

The 4KScore test has already been launched in Europe and is expected to be launched in the US in 2013. Opko’s recent acquisition of OURLab provides the company with 18 phlebotomy sites in the US, with a national sales force that calls on urologists.

Ongoing sales of competing PSA tests suggest that the revenue potential for this market is indeed quite large. However, investors in Opko do need to temper their optimism with some amount of realism in terms of what to expect and when, in terms of sales of prostate cancer diagnostic tests.

The sales force will no doubt help the marketing effort for the 4KScore, but it cannot increase the test’s ability to actually detect prostate cancer.

There are two issues that investors should consider when making their revenue forecasts: competition and emerging medical trends regarding PSA testing. As for competition, Opko will certainly not be the first company to launch a revolutionary new PSA based test and then see its stock price soar. As noted in the New York Times quite a few years ago:

The stock price of Biomerica Inc. quadrupled yesterday after the tiny medical technology company said it would produce a five-minute test for the diagnosis of prostate cancer. … The company said it would first sell the test outside the United States and would begin sales here if it received clearance from the Food and Drug Administration…..Biomerica’s shares soared $7.375, or 311 percent, to close at $9.75 on volume of 3.6 million shares in Nasdaq trading.

As with Opko, Biomerica’s EZ-PSA prostate cancer test was first launched outside of the US and was subsequently approved in Japan as well. The EZ-PSA test is still commercially available. However Biomerica (BMRA) never had blockbuster success from the test. Biomerica’s stock has now traded down to $1.20 and has a market cap of just $8 million.

Biomerica actually bears some similarities to Opko and describes it business as:

Biomerica, Inc.(Biomerica), develops, manufactures, and markets medical diagnostic products designed for the early detection and monitoring of chronic diseases and medical conditions.

The company will do close to $8 million in revenues this year, and with a market cap of just $8 million and no debt it actually appears to be a very interesting speculative buy.

Competition has meant that the prices of PSA tests have come down substantially, with some test centers providing various tests for as low as $49.00.

In assessing revenue prospects for Opko’s 4KScore, some bullish authors have assumed that Opko will immediately capture a 50% market share while simultaneously charging triple the price for PSA tests. The result was $1.8 billion in annual revenues expected by a recent author.

Each investor will have his or her own individual method of forecasting, however using more realistic assumptions for price (below $100) and market share (15-20%) would yield a number that is at most $200-300 million. This is still a considerable amount of revenue to realize from a new product, however investors do need to realize that such estimates fall around 85% below the $1.8 billion level that many seem to be hoping for.

Author Josh Ginsberg recently estimated that Opko would be realizing as much as $8.3 billion per year based on the 4KScore and Opko’s near term drug prospects. In doing so, he quoted the $1.8 billion forecast for 4K from another author.

However Mr. Ginsberg does suggest that individual readers conduct their own due diligence in arriving at such estimates.

Some of the competition may not come from competing PSA tests at all, but instead will come from competing non-PSA technologies.

According to a 2012 article in MedCity News:

Armune Bioscience Inc. is developing a test based on serum autoantibodies,which the company says are more stable than antigens and may be easier to detect during early stage cancer. First, the company is focusing on creating analternative to the low-specificity, prostate-specific antigen test that’s the current standard for detecting prostate cancer.

The company has already raised over $3 million from investors to develop the test.

According to a 2012 article in Fierce Biomarkers:

Beckman Coulter (DHR) has received premarket approval from the FDA for its biomarker-based Prostate Health Index (PHI). According to the company, this test is 2.5 times more specific in detecting prostate cancer than PSA (prostate-specific antigen) tests in men with raised levels of PSA, and could cut the number of unnecessary prostate biopsies 31%.

In addition, Quest Diagnostics (DGX) currently offers a urine based screening test for prostate cancer.

Medical pushback against prostate cancer testing

In reality, a much bigger potential impediment to Opko realizing 4K’s full revenue potential could be the increasing amount of backlash that PSA tests are facing from the medical community. The backlash against PSA testing has been building for two years now and seems to have escalated substantially in 2012.

These criticisms are coming from many of the most respected names in the medical field with respect to prostate cancer. Surprisingly they are calling for a near halt to the widespread use of PSA tests used as an advanced screener.

The PSA test was actually invented by Dr. Richard Albin. In a New York TimesOpEd piece entitled “The Great Prostate Mistake” Dr. Albin decried the currentover-use of PSA tests as:

“a profit-driven public health disaster.”

Later, an article entitled “PSA Screenings: a Money-Making Scam” went even further to hammer home the same point.

Most recently, the backlash against PSA testing seems to have come to a head in much broader medical circles. The San Francisco Chronicle noted that:

many possible screening programs turn out not to do any good – and in fact some tests like PSA cause harm. That’s why virtually all expert public health panels do not recommend the PSA test.

Also in 2012, an article entitled “Harvard expert urges caution for use of new prostate cancer test” raised similar concerns. Each of these authors raises a wide range of points which suggest that the problems with PSA testing outweigh the benefits for many of the men who end up getting the test done. The authors go on to strongly criticize the industry for over promoting PSA tests in pursuit of profits.

They suggest that the appropriate target market should consists primarily of men who have already had prostate surgery, rather than as a predictive measure performed in advance. Clearly such a shift would result in a very dramatic reduction in the size of the addressable market.

For now it seems safe to say that PSA tests will continue to be widely used for the foreseeable future. However the increasing trend in the medical community to curtail their use should certainly be considered as a factor by those who are expecting multi-billion dollar revenues from 4KScore alone and in the very near term.

Such investors should also keep in mind the strong cautionary comments raised by the medical community specifically with respect to Opko’s prostate cancer test, as was highlighted in Barron’s.

Playing the short squeeze

Even when the share price was just over $4.00, the short interest in Opko was enormous. During 2012 the short interest in the stock typically ranged from 30-32 million shares, so about 25% of the outstanding share count at the time.

The bet on the short side was premised on the fact that at $4.00 Opko was still a $1.2 billion company with almost no revenues and with losses that were increasing substantially each quarter.

Much of the recent surge in the share price can be clearly attributed to short sellers scrambling to cover.

We can see from the Nasdaq that the overall short interest has now fallen by nearly 30%. Meanwhile the number of days to cover the short interest has fallen from 43 days in August to just 11 days at present. The short in Opko was very large, but is now very moderate.

As a result, short covering cannot be expected to continue to prop up the share price going forward, and in fact shorts will likely begin re-entering the stock at current levels.

| Settlement Date | Short Interest | Avg Daily Share Volume | Days To Cover |

| 1/15/2013 | 23,901,216 | 2,174,211 | 10.993053 |

| 12/31/2012 | 24,263,036 | 1,262,059 | 19.224962 |

| 12/14/2012 | 29,785,788 | 1,456,180 | 20.454743 |

| 11/30/2012 | 31,705,090 | 1,067,204 | 29.708556 |

| 11/15/2012 | 32,320,163 | 1,636,147 | 19.753826 |

| 10/31/2012 | 31,845,538 | 1,178,310 | 27.026451 |

| 10/15/2012 | 30,818,850 | 1,179,777 | 26.122606 |

| 9/28/2012 | 31,105,015 | 1,102,191 | 28.221075 |

| 9/14/2012 | 31,612,311 | 753,306 | 41.964767 |

| 8/31/2012 | 31,243,465 | 844,779 | 36.984188 |

| 8/15/2012 | 31,220,187 | 719,274 | 43.405138 |

Conclusion – knowing when to take profits and when to re-enter

Share of Opko have been on a spectacular run and have been boosted by a series of simultaneous positive factors including:

- The positive signaling effect from Dr. Frost’s small purchases

- Ample positive attention from Jim Cramer

- A notable short squeeze

- Ongoing enthusiasm from bullish authors with ultra bullish revenue forecasts

However with a market cap of over $2 billion, the stock is clearly one of the most overvalued names in the healthcare space relative to its actual revenue prospects over the next 2-3 years.

The only new near term revenue event will be the market launch of the 4KScore in the US in coming months. Realistically revenues from the 4K product may be around 85% lower than what has been predicted by bullish authors, and will certainly take time to ramp up even to that reduced level.

Opko itself has cautioned investors that it does not expect to become profitable in the near term, which basically tells us that any potential billion dollar revenue events are still expected to occur much further out than many authors are currently forecasting.

The near term signals of an impending correction in the share price include:

- The onset of insider selling of shares by management / insiders

- The signaling effect of over 45 million of new shares being issued by Opko in January alone

- The overhang from the convertible and from the shares issued to acquisition targets

- A sharp decline in short interest such that the short squeeze will no longer be supporting the share price

At prices any prices over $5.50, Opko isn’t just a good short, it is a great short. But once the share price pulls back to the $4.00-$5.00 range it likely becomes an interesting buy and hold stock for some time, depending on how results begin to shape up in 2013-2014.

Disclosure: I am short OPK. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.